Connector Series 2022 - Outlook

Outlook

As referred to above, demand is under immense pressure. If the drivers of the multi-factor crisis gain further momentum, IMF sees their growth projections for the world economy at risk of being further reduced. Their downside risk scenario to their already downward corrected assumptions of 3.2% and 2.9% growth for 2022 and 2023 are 2.6% (2022) and 2.0% (2023).

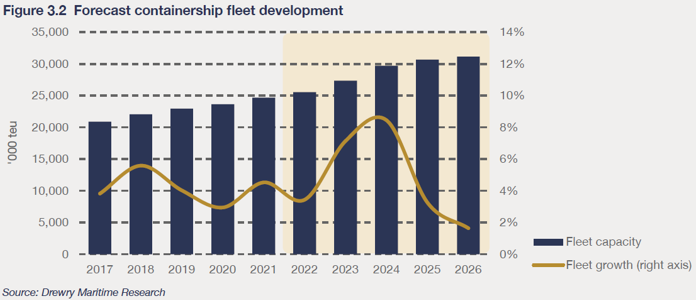

Supply forecasts can be made with more confidence due to the ship orderbook visibility and the nature of the delay it takes to build the ships. Hence, most interesting in terms of the orderbook is the delivery schedule and as such the question when the massive influx of brand-new tonnage will hit the water. As per Drewry’s latest forecast, this will start in 2023:

While this massive capacity growth is currently looking to coincide with a dramatic erosion of demand in an environment of substantial uncertainty, the carriers still seem to be comparably relaxed about the situation. Reasons for this are firstly the tight capacity management tools they have at hand. Slow steaming might have been taken as far as ship operations allow, but by starting to scrap aged tonnage again and artificially keeping supply temporarily tight by idling ships, carriers can take millions of TEU out of the market at relatively short notice. Furthermore, an order placed by a shipping line does not mean it cannot be cancelled with the ship building yard or delivery of the ships delayed by years. Shipping lines have always been opportunistic in this regard and with their increased profit awareness, they will likely prefer playing those cards over intentions to secure market share. The carriers are cash richer than ever and many of them have diversified into landside logistics offerings, airfreight, or technology, which will allow them to weather a market turning to their disadvantage better than ever before. Secondly, port congestion, as one of the main reasons for capacity tightness, is not expected to disappear anytime soon. Without that disruptor continuously causing bottlenecks, the situation would be dramatically different. But Covid numbers are flaring up again, lockdowns for example in China can happen at any time and inflation leads to further labour shortages, when for example port workers go on strike to fight for higher wages, with congested German ports as a result being just one recent example.

In the prevailing global economic climate and deriving container shipping environment it is impossible to tell how the rates will develop further and when the operational landscape of container shipping, ports, and logistics globally as well as here in New Zealand will improve.

All things considered; the carriers will likely remain in a strong negotiation position for another 9 to 12 months. It is a possible assumption that mid 2023 will mark a turning point in the power balance of shippers and shipping lines. The indicators suggest that, but it cannot be underlined enough that the uncertainties around all drivers are abundant. In its latest Container Forecaster, Drewry expects global freight rates to increase by 37% in 2022, with spot rates declining but staying relatively strong and contract rates expected to hold up well into 2023. Should the power shift happen halfway through 2023, rates are expected to decline by 33% for the full year 2023 as a mix of opportunities to negotiate contract rates down and weaker spot rates, however, still expected to stay very comfortably far above pre-pandemic levels.

Summary

This in mind, in New Zealand we expect a continuous challenging environment to persist as we continue to deal with supply chain meltdowns in various areas around the globe. As a consequence of high freight rates, the trades keep competing for vessel deployment and equipment supply. Shipping lines keep taking radical decisions to maximise profits and since shipping services connecting New Zealand to the world often require transhipment in ongoing operationally constrained or heavily congested ports to reach equally congested outports, we are exposed to cuts in the service offering or substantial rate increases – or both. At the same time, New Zealand customers across the board have been forced to accept drastically reduced service levels in the form of multiple rollings, largely unpredictable transit times or even plain deselection and cancellations and we do not expect this environment to change anytime soon.

To achieve the best results for our customers, address the ongoing operational constraints in New Zealand and start negotiations on the upcoming new contract period, we took advantage of the re-opening borders and immediately travelled overseas in May and June to meet face to face with the shipping lines’ decision makers in Australia, Asia, and Europe. Furthermore, we welcomed overseas trade managers as well as regional and domestic heads of the different carriers in New Zealand to discuss further.

The meetings were as diverse as the shipping world itself. Most partners were very welcoming, open, and approached the challenges and concerns we confronted them with in our meetings with a constructive and collaborative approach and mindset. However, we also had to experience strong examples of arrogance, complacency, and sheer ignorance towards the impact global or regional headquarters’ decisions have on regional markets and in part faced aggressive headwinds on our suggestions of how an improved collaboration to the benefit of our customers and New Zealand’s competitive position in the world going forward could look.

To avoid operational disruptions to your supply chains in these ongoing trying times as much as possible, we would like to again ask you to place bookings as early and far in advance as possible on our portal in order to mitigate operational risks and build resilient inventory levels. Thank you for your co-operation and support, which we value very highly. We would like to reassure you that our teams and our service providers are working tirelessly on solutions to provide you the best possible customer service in order to keep the impact on your operations, and those of your customers as limited as possible.